Science fiction movies and books may portray artificial intelligence as a human-like giant brain with thousands of wires coming from it that control whole cities and their populations. The reality today is that artificial intelligence is unobtrusive, everywhere, and we are interacting with it multiple times daily without always recognizing that we are.

Science fiction movies and books may portray artificial intelligence as a human-like giant brain with thousands of wires coming from it that control whole cities and their populations. The reality today is that artificial intelligence is unobtrusive, everywhere, and we are interacting with it multiple times daily without always recognizing that we are.

Artificial intelligence is being used by large corporations in a range of areas, including sales, marketing, customer service, employee training/coaching, and logistics. Small businesses can also employ artificial intelligence to improve customer service, reduce costs, and help drive revenues.

What It Is

Artificial intelligence (AI) is a branch of computer science that focuses on building smart machines capable of performing tasks that typically require human intelligence. Essentially, it endeavors to simulate human intelligence in machines. Examples of AI applications many people are familiar with include smart assistants (such as Siri and Alexa) and virtual agents that interact with customers and guide them to possible solutions. Looking ahead, self-driving trucks and cars are in various stages of development, and some vehicles already have self-driving features.

Customer Service

AI can be deployed through the use of chatbots to handle a variety of tasks, such as directing callers to the function they want (e.g., automatic payments). On a more complex level, AI can be used online to help customers with product search and discovery and respond to requests with relevant recommendations. Businesses can use data gathered from AI chatbot customer interactions to identify where in the process problems may arise and what these problems are so that they can be eliminated in the future.

Logistics

Moving goods from one point to another requires up-to-the-minute data so that what is being shipped is shipped in the most efficient and cost-effective way possible. Certain AI programs can predict points where congestion may happen and help redirect trucks and vans so that they avoid bottlenecks and slowdowns. AI essentially streamlines the supply chain. It can do something similar when it comes to warehouse management — identifying choke points that slow the movement of goods from point A to point B.

Marketing

AI marketing sets out to leverage customer data and machine learning to anticipate a customer’s next move and to nudge that customer toward either buying something or increasing his or her average order value. Businesses are using AI to attract, nurture, and convert prospects.

By tracking a customer’s online searches, AI programs can identify what products an individual might be interested in and may be considering buying. AI can target that individual with ads highlighting products or services previously identified as being of interest to the customer. This approach essentially uses machine learning to offer personalized product recommendations.

Sales Training

AI can be used to coach salespeople to improve their sales skills and help them increase their percentage of successful sales calls. AI programs exist that can analyze a number of variables that are used by the most successful salespeople and use that data to identify strategies that can be replicated and utilized by other salespeople within the organization.

As with any technology, there are costs involved in incorporating AI into a company’s operations. A financial professional can assist you in analyzing the costs and potential financial benefits of any new technological enhancements your small business may be considering.

With gas prices so high, you need to track your travel costs as closely as possible. Consider getting a tax deduction for your business mileage.

With gas prices so high, you need to track your travel costs as closely as possible. Consider getting a tax deduction for your business mileage.

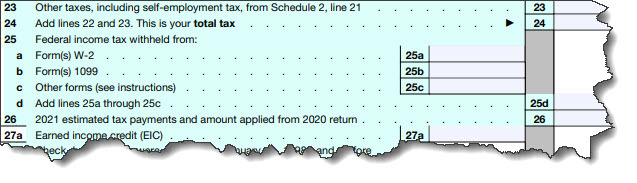

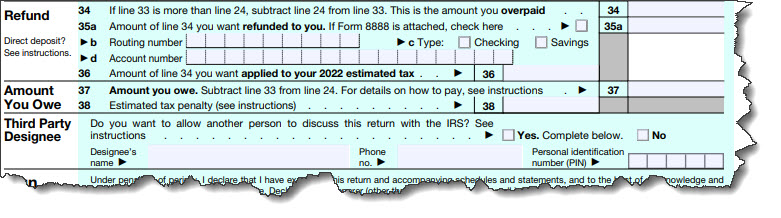

Did you skip filing or request an extension on your 2021 taxes because you couldn’t pay? You have several options.

Did you skip filing or request an extension on your 2021 taxes because you couldn’t pay? You have several options.

As a small business owner, tax liability is the money you owe the government when your business generates income. With changing laws and gray areas regarding deductions, exemptions, and credits, it’s no wonder small business owners rank taxes at the top of the list of the most stress-inducing aspect of business ownership. To reduce that stress, taxes shouldn’t be something to focus on only at year’s end. Use these tips on reducing your business tax year-round and see your taxes and stress level decrease!

As a small business owner, tax liability is the money you owe the government when your business generates income. With changing laws and gray areas regarding deductions, exemptions, and credits, it’s no wonder small business owners rank taxes at the top of the list of the most stress-inducing aspect of business ownership. To reduce that stress, taxes shouldn’t be something to focus on only at year’s end. Use these tips on reducing your business tax year-round and see your taxes and stress level decrease! Comparing a business’s key financial ratios with industry standards and with its own past results can highlight trends and identify strengths and weaknesses in the business.

Comparing a business’s key financial ratios with industry standards and with its own past results can highlight trends and identify strengths and weaknesses in the business. It’s not just self-employed individuals who must pay estimated taxes. Here’s what you need to know.

It’s not just self-employed individuals who must pay estimated taxes. Here’s what you need to know.